INTRODUCTION

Global expenditure on medicines has risen in recent years. Expenditure of medicines is expected to reach US$1.5 trillion by 2023, which represents an annual compounded growth rate of 3%–6% (IQVIA, 2019a). This increase in expenditure is driven by a number of factors. These include increasing expenditure on biologicals for orphan diseases and cancer, a growing prevalence of non-communicable diseases (NCDs) and changes in clinical practice (Godman et al., 2018a, 2021a). We are aware that approximately one fifth of health care spending in Europe is out-of-pocket, with the proportion greater among those patients with low income (OECD, 2020; Thomson et al., 2019).

High patient co-payments and reimbursement issues with biologic medicines have resulted in many Central and Eastern European (CEE) countries struggling to fund originator biologic medicines (Baumgart et al., 2019; Tubic et al., 2021). Rencz et al. (2015) found only 0.25% of all patients diagnosed with psoriasis were treated with biologics among six researched CEE countries, with a 14.6-fold difference in utilization rates between them (Rencz et al., 2015). There have also been similar disparities with medicines to treat patients with orphan diseases and cancer across Europe (EURODIS, 2018; Hofmarcher et al., 2019). This urgently needs addressing to ensure equitable healthcare for all across Europe, especially with rising rates of NCDs and concerns with unequal funding for priority disease areas such as diabetes (Godman et al., 2018a, 2021b; Mardare et al., 2022).

Biosimilars should be of interest to improve access, affordability, and subsequent care of patients (Cozijnsen et al., 2018; Dutta et al., 2020; Godman, 2021; Jang et al., 2021). Davio (2018) estimated accumulated savings from the increasing use of biosimilar etanercept, infliximab, and rituximab biosimilars in the UK was US$275 million during the 2017 to 2018 fiscal year (Davio, 2018). However, there are concerns with biosimilar use in some countries, which includes issues with their effectiveness and safety (Godman, 2021; Sagonowsky, 2019; Vandenplas et al., 2021). This is reflected by the usage of anti-TNF biosimilars for rheumatology patients ranging from 90% of all anti-TNFs in Denmark by the end of 2016 to just 5% in Belgium and Ireland and 2% in Switzerland (Araújo et al., 2019). Similarly, in another study, their utilization ranged from 0% of total anti-TNFs in Hungary up to 81% in Norway and 96% in Denmark (IQVIA, 2019b).

There have also been issues with administering biosimilars of long-acting insulin analogues among European countries (Chapman et al., 2017; Greener, 2019; Godman et al., 2021c). This is a concern with the costs of diabetes and associated complications reaching up to 2.2% of Gross Domestic Product by 2030 (Bommer et al., 2018). Long-acting insulin analogues were developed to reduce hypoglycemia, including nocturnal hypoglycemia, among patients with diabetes requiring insulin (Rys et al., 2015; Tricco et al., 2021). There have though been concerns regarding their additional costs compared with insulins such as NPH insulins (Caires de Souza et al., 2014; Ewen et al., 2019). However, these extra costs can be offset by savings elsewhere (Godman et al., 2021c; Lee et al., 2020). As a result of these potential cost offsets, coupled with their perceived patient benefits, long-acting insulin analogues have become the most utilized insulin in upper-middle and high-income countries (Ewen et al., 2019). The costs of long-acting insulin analogues can be reduced by the availability of biosimilars (Haque et al., 2021a). However, the originator company has been promoting the patented high concentration 300 IU/ml formulation of insulin glargine (Gla-300) to protect their overall insulin glargine sales as well as reduce the price of 100 IU/ml formulation to reduce the attractiveness of this market for biosimilar manufacturers (Godman et al., 2021b; Tubic et al., 2021).

Consequently, we believe there is a need to consolidate current knowledge regarding measures to enhance biosimilar use and their impact across Europe. In addition, look more closely at the situation with insulin glargine across Europe as the first in class biosimilar given concerns with its initial uptake coupled with the need to conserve resources. The combined findings can be used to guide key stakeholder groups on potential ways in the future to enhance biosimilar utilization, including insulin glargine biosimilars, across Europe and wider. This is seen as vital to encourage greater competition among biosimilar manufacturers to benefit all key stakeholder groups given rising expenditure on medicines and concerns with the need to preserve universal healthcare among European countries. This includes patients with diabetes requiring long-acting insulin analogues where costs and available resources are a concern. We believe these findings can also be of benefit to low- and middle-income countries struggling to finance healthcare for all their citizens in the public sector including patients with diabetes (Godman et al., 2020a, 2020b; Haque et al., 2021b; Mardare et al., 2022).

METHODS

A mixed-method approach was adopted. This included initially a narrative review of published studies regarding biosimilars, including initiatives that have been used among countries to enhance their use. This was combined with cross national quantitative and qualitative research among European countries, especially CEE countries, regarding their utilization and expenditure on long-acting insulin analogues with a particular focus in insulin glargine and its biosimilars.

Narrative literature review

We undertook a narrative review of published studies. This included documenting the impact of demand-side measures that had been instigated among European countries, including CEE countries, to enhance uptake and prescribing of biosimilars. In addition, studies where there had been limited use of biosimilars and the rationale. We did not undertake a systematic review as there have been previous studies exploring these issues. This includes documenting the efficacy, safety, and immunogenicity of switching between biosimilars and originators, coupled with the key benefits of biosimilars, and we wanted to build on this (Barbier et al., 2020; Bertolani and Jommi, 2020; Dutta et al., 2020; Godman 2021; Godman et al., 2021a, 2021d; Kim et al., 2020). The documented examples are based on the considerable knowledge of the senior level co-authors and subsequently contextualized.

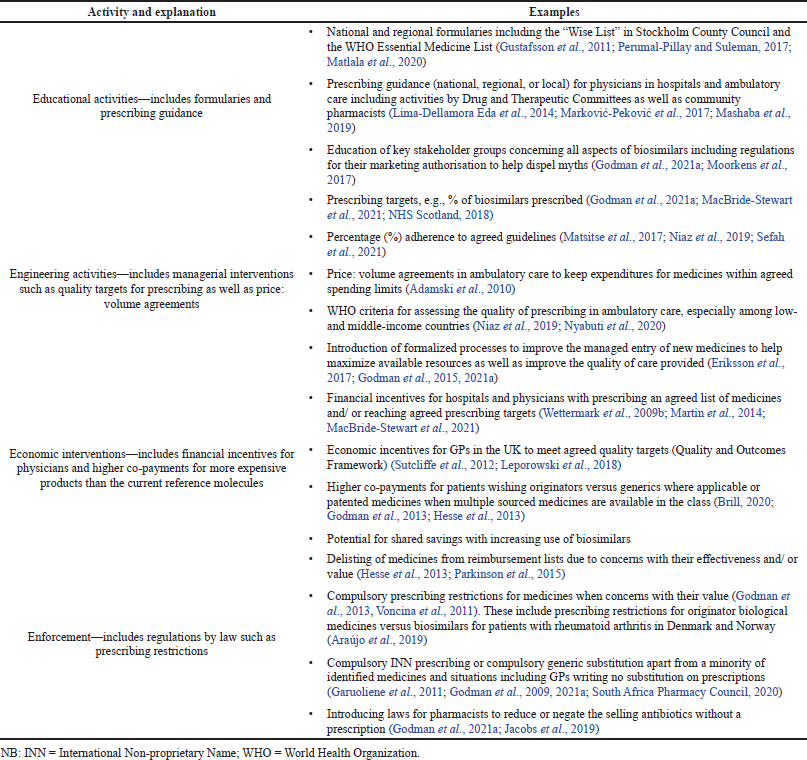

The demand-side measures will be collated under the Education, Engineering, Economics, and Enforcement (4Es) to aid comparisons (Wettermark et al., 2009a). Table 1 provides definitions and examples of the 4Es.

This is similar to approaches that have been used when debating key areas principally from a health authority perspective (Bochenek et al., 2017; Godman et al., 2018a, 2021a, 2021e, 2021f, 2021g; MacBride-Stewart et al., 2021).

Cross national drug utilization and expenditure study

This study principally concentrated on CEE countries given concerns with the utilization and funding of higher price biological medicines in these countries (Baumgart et al., 2019).

The CEE countries chosen for this study provide an extensive range based on their population size, geography and economic power (Godman et al., 2019a). We also included three high income Western European countries and regions for comparison purposes. These were Italy, Spain (Catalonia), and the UK (Scotland); chosen as the health authorities in these countries have instigated multiple measures to enhance the prescribing of biosimilars (discussed in Table 2). We limited Western European countries to these three as the main focus of this paper was on CEE countries.

Heath insurance company and health authority databases were principally interrogated from 2014 or later until 2020 to determine pricing, expenditure, and utilization patterns principally for the different insulin glargine preparations. These databases were chosen as they are seen as robust and are audited regularly (Godman et al., 2019a, 2019b, 2021b; Vogler and Schneider, 2019). The findings were used to determine changes in utilization patterns for long-acting insulin analogues during the study period as well as changes in the utilization of biosimilars of insulin glargine during the study period. In addition, price changes for both originator and biosimilar insulin glargine over time.

Defined daily doses (DDDs) were used where possible for utilization to enhance the comparisons between countries, with DDDs recognized as a robust measure for undertaking cross-country utilization research (Godman et al., 2014, 2021f, 2021h; Tubic et al., 2021).

Principally reimbursed pricing and expenditure data was used as the perspective of this paper is that of health authorities. This approach has been used before to provide comparisons between European countries (Godman et al., 2014, 2019a). Expenditure data remained in the local currency where relevant in order to avoid potential biases due to currency fluctuations. This is because we were principally interested in percentage differences over time for both the biosimilars and originators, as well as any price reductions for both of them over time, rather than absolute pricing levels.

Qualitative research regarding insulin utilization patterns

The senior-level co-authors from each of the studied countries were approached to provide feedback regarding the possible rationale for the insulin utilization and expenditure patterns seen. They were also approached to provide guidance on possible next steps that could be instigated among European countries to enhance savings from the increased use of biosimilars. We have used similar approaches in the previous publications (Bochenek et al., 2017; Godman et al., 2019a, 2021a, 2021e, 2021f, 2021g, 2021h; Haque et al., 2021b).

We did not seek ethical approval for this study as we were not dealing directly with patients. This is in agreement with national legislation and institutional guidelines. In addition, endorsed in previous publications which have involved the co-authors (Godman et al., 2019a, 2021b; Hesse et al., 2013, Tubic et al., 2021).

RESULTS

We will first document initiatives regarding biosimilars and their impact before discussing the patterns seen regarding utilization and expenditure for long-acting insulins, including biosimilars, during the study period.

Initiatives to enhance the utilization of biosimilars and their impact

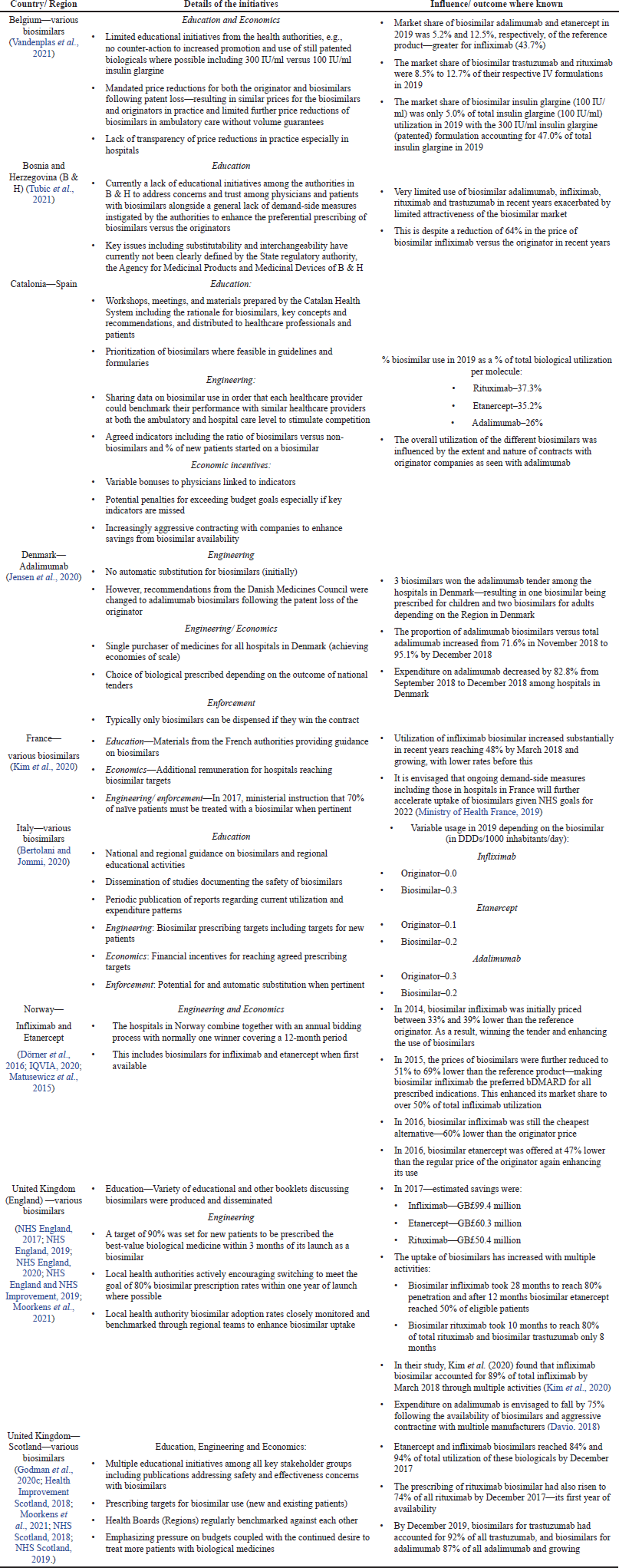

Table 2 documents the wide range of demand-side measures that have introduced by different European countries and their influence collated under the 4Es.

Long-acting insulin analogues including insulin glargine

Utilization and expenditure patterns

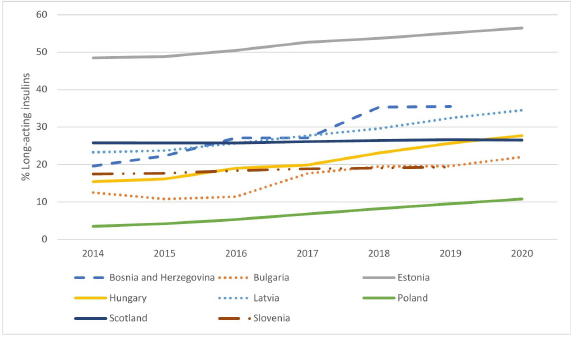

There has typically been growing expenditure and utilization of long-acting insulin analogues as a percentage of total insulins among the European countries included in this study (Figs. 1 and 2). The greatest increase in utilization among CEE countries was seen in Poland; however, this was from a low base. By 2020, the highest percentage utilization of long-acting insulin analogues among the studied European countries was seen in Estonia (56.5% of total insulins) followed by B & H (35.5%). There was also considerable usage in Catalonia at 55.2% of total utilization.

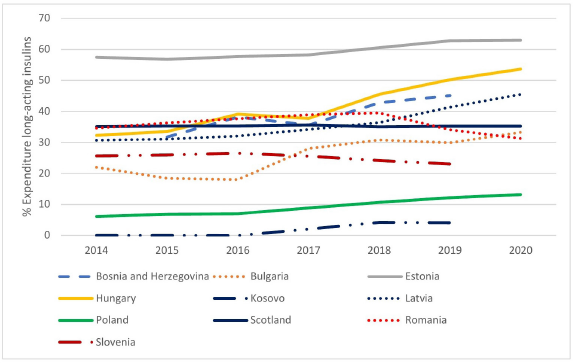

There were similar findings when comparing the change in percentage expenditure on long-acting insulin analogues versus total expenditure on insulins during the study period (Fig. 2). However, typically a greater percentage reflecting higher acquisition costs for insulin analogues despite price reductions.

| Table 1. Explanation and examples of health authority activities to influence medicine utilization—4Es. [Click here to view] |

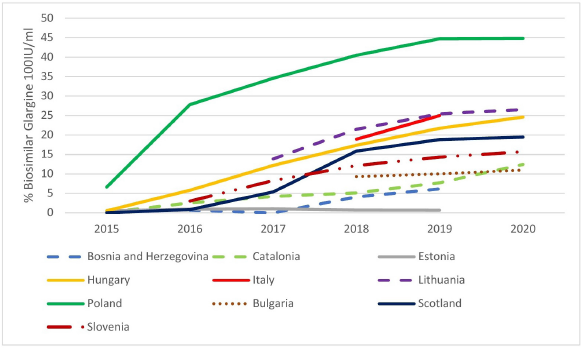

We also saw a considerable variation in the prescribing of biosimilar insulin glargine compared with total insulin glargine across Europe (Fig. 3).

Rationale for differences in utilization and expenditure patterns

The differences in the utilization patterns for biosimilar insulin glargine (Fig. 2) have in part been driven by the originator company promoting patented Gla-300 as well as lowering the price of originator 100 IU/ml (Table 3) to compete. These combined activities alongside limited demand-side measures (Table 4) have been successful with no biosimilar 100 IU/ml insulin glargine launched to date in Albania or Latvia as well as limited use in Bulgaria, B & H, Estonia, Romania, and Slovenia. These findings of limited or no use of biosimilars to date contrast with growing utilization of biosimilar insulin glargine in the other studied European countries, i.e., Lithuania, Hungary, Poland, and Scotland, with the greatest utilization seen in Poland.

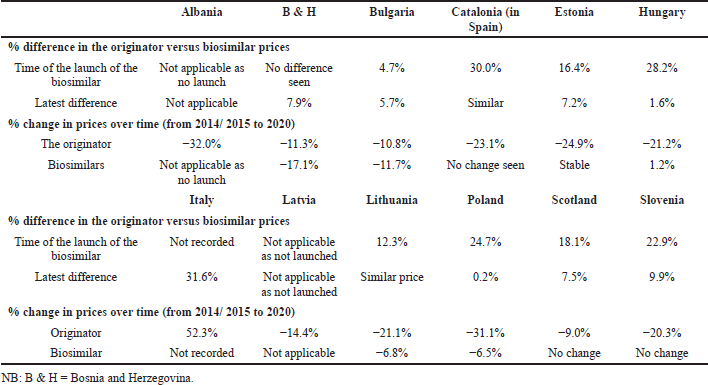

Table 3 documents price changes over time of the different insulin glargine preparations (100 IU/ml) among the studied countries.

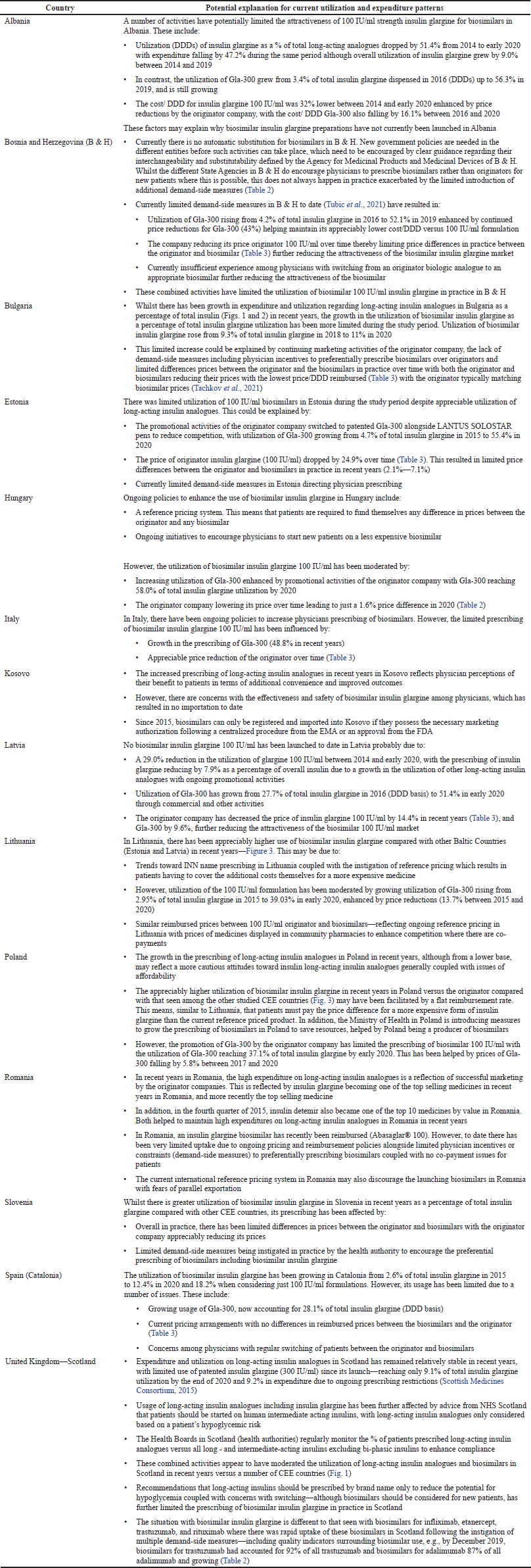

Table 4 provides a summary of the rationale for the changes seen in Figures 1–3 as well as Table 3.

DISCUSSION AND THE IMPLICATIONS

We will break the discussion down into the implications of the findings for the biosimilar market in general and subsequently for the biosimilars for long-acting insulin analogues in particular, with the aim of benefiting of all key stakeholder groups in the future.

| Table 2. The extent of demand-side measures that have been instigated influence biosimilar use among European countries and their impact where known [adapted from (Godman et al., 2021a, 2020c; Godman, 2021; Kim et al., 2020)] [Click here to view] |

| Figure 1. Utilisation of long-acting insulin analogues over time among selected European countries and Regions as a percentage of total insulins (DDD based) [Click here to view] |

| Figure 2. Expenditure on long-acting insulin analogues over time as a percentage of total insulin expenditure among selected European countries and Regions [Click here to view] |

| Figure 3. Utilisation of insulin glargine biosimilar (100IU/ml) as a % of total insulin glargine 100IU/ml (DDD basis) among selected European Countries and Regions [Click here to view] |

| Table 3. Price differences for both the originator and biosimilar 100 IU/ml over time among the different European countries. [Click here to view] |

Biosimilar market (General)

Among European countries, there have been considerable disparities in the prescribing of biosimilars in recent years (Table 2) as well as among Asian countries. These differences have been driven by concerns with their safety and effectiveness, limited price differences in practice between originators and biosimilars in a number of countries alongside limited instigation of demand-side measures to increase their prescribing (Godman et al., 2021a, 2021e; Kim et al., 2020; Moorkens et al., 2017; Tubic et al., 2021).

The instigation of multiple demand-side measures, along with greater price differentials, can appreciably enhance the uptake and use of biosimilars (Table 2). This mirrors the situation that has been seen with multiple-sourced oral medicines where the instigation of multiple demand-side measures has appreciably enhanced their preferential prescribing versus patented medicines in a class where this did not compromise care (Godman et al., 2014, 2018b, 2019b, 2021a, 2021d; Leporowski et al., 2018; Martin et al., 2014). In addition, the situation seen with antimicrobials where sustained implementation of multiple demand-side measures enhanced their appropriate prescribing among former Soviet Union Republics including CEE countries compared to continually increased utilization without such measures (Godman et al., 2021a, 2021g).

| Table 4. Potential rationale for the expenditure and utilization patterns seen for the different insulin glargine preparations seen among the studied European countries. [Click here to view] |

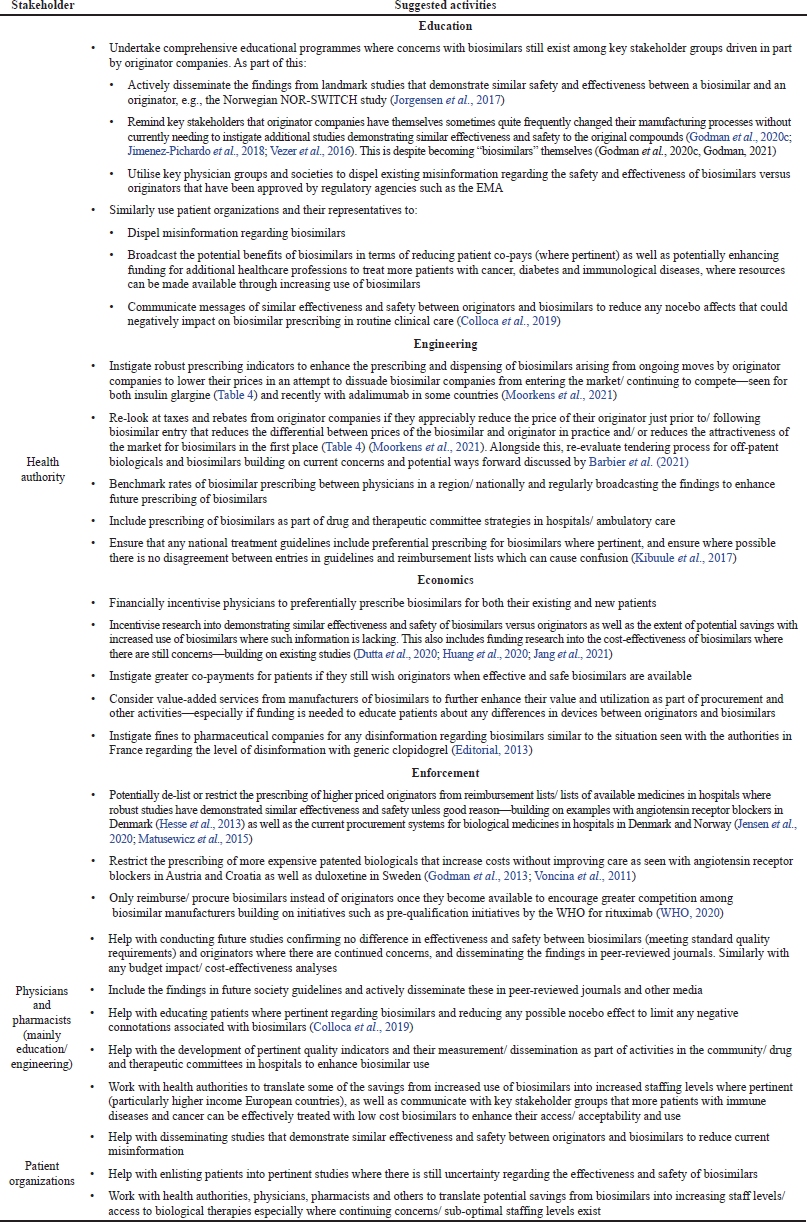

Table 5 discusses potential measures that could be introduced among all key stakeholder groups across countries, broken down by the 4Es where pertinent (Table 1), to enhance the prescribing of biosimilars where issues and concerns still exist. This builds on the findings in Tables 2 and 4 alongside the considerable experience and expertise of the senior level co-authors. It is recognized by all key stakeholders that it is important to increase the prescribing of biosimilars, especially in countries with universal healthcare. This is because attempts to reduce their prescribing will make the biosimilar market unattractive and compromise the future funding of medicines (Godman et al., 2021a, 2021d). This will be detrimental to all key stakeholder groups in the coming years especially given the appreciable number of biologic medicines that are likely to soon lose their patents coupled with the need to fund new high priced medicines that address current unmet needs (Godman et al., 2021a, 2021e).

Biosimilar long-acting insulin analogues

Insulin glargine is a different situation to the biosimilars of anti-TNF alphas, as well as adalimumab, rituximab, and trastuzumab in terms of increasing expenditure and use of long-acting insulin analogues among CEE countries (Figs. 1 and 2). This contrasts with previous low use of biological medicines to treat patients with immunological and oncological diseases in these countries (Baumgart et al., 2019; Godman et al., 2021a). This growing use reflects increasing recognition of the value and role of long-acting insulin analogues in managing patients with diabetes across countries although there can still be issues with affordability in some countries (Ewen et al., 2019; Godman et al., 2021g; Haque et al., 2021a, 2021b; Tricco et al., 2021).

There are though concerns with the low use of biosimilar insulin glargine in practice (Fig. 3) in a number of European countries versus the high use of biosimilars generally (Table 2).

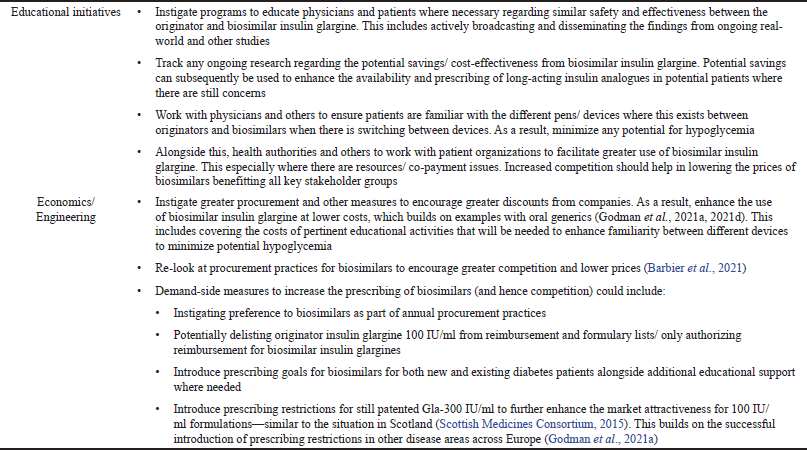

The low use of biosimilar insulin glargine in a number of European countries (Fig. 3) may be due to a number of factors. These include the originator company lowering the price of 100 IU/ml insulin glargine and switching promotional efforts to Gla-300 (Tables 3 and 4). The situation with the manufacturer of originator insulin glargine switching promotion to the higher strength patented 300 IU/ml formulation is similar to previous evergreening activities by companies (Alkhafaji et al., 2012; Vernaz et al., 2013). Examples include switching promotion from omeprazole to esomeprazole and citalopram to escitalopram, increasing costs without necessarily improving patient care (Godman et al., 2018b, 2019b; Vernaz et al., 2013). Table 6 builds on Table 5 to review a number of activities that can be undertaken by key stakeholder groups across Europe to enhance future utilization of biosimilar insulin glargine 100 IU/ml. The instigation of such activities should encourage more companies and formulations of biosimilar long-acting insulin to launch new biosimilars. As a result, helping to lower prices, which should benefit all key stakeholders. It is also important for European health authorities to encourage companies to develop biosimilars for insulin glargine as this will help them justify investment to develop biosimilars for still patented long-acting insulin analogues. This will again benefit all key stakeholder groups across countries with growing prevalence rates for patients with diabetes. We will continue to monitor this.

| Table 5. Potential strategies among all key stakeholder groups to enhance the prescribing of biosimilars across Europe where issues and concerns still exist. [Click here to view] |

| Table 6. Potential activities among European health authorities to enhance the prescribing and dispensing of insulin glargine biosimilars. [Click here to view] |